Securing a mortgage has always been a significant milestone in achieving the dream of homeownership. However, for self-employed individuals, this journey can be fraught with unique challenges and complexities.

In this comprehensive guide, we will explore the key steps and strategies for self-employed individuals to successfully secure a mortgage in 2024.

Importance of Financial Stability for Mortgage Approval

One of the foremost considerations when applying for a self-employed mortgage is demonstrating financial stability. Lenders want assurance that you can meet your monthly mortgage payments consistently. To achieve this, it’s crucial to maintain well-organized financial records.

This includes documenting your income, expenses, and profits over an extended period, typically two years or more. Consistency in your financial stability is a reassuring sign for lenders, making them more willing to approve your self-employed mortgage application.

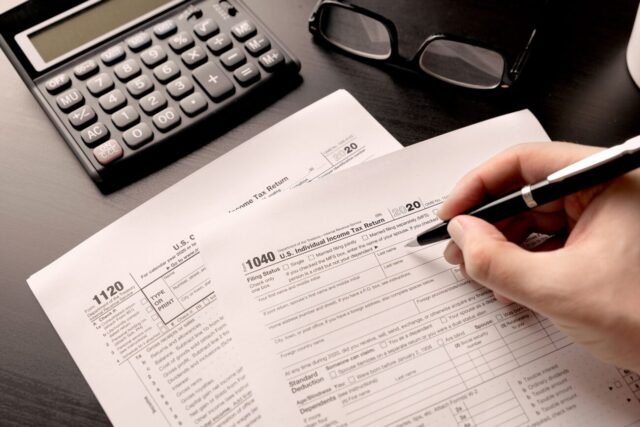

Tax Returns and Documentation Requirements

Tax returns and documentation requirements are pivotal when self-employed individuals seek approval. Lenders scrutinize tax returns, typically spanning two or more years, to assess income consistency and viability. Unlike traditional employees with straightforward W-2 forms, self-employed applicants often present Schedule C or Schedule K-1 documents, detailing business income and deductions.

Clear and accurate documentation is essential. Self-employed borrowers must maintain well-organized records, including bank statements and profit and loss statements. Any income fluctuations should be explained, helping lenders understand the stability of your finances.

In essence, tax returns and related documents serve as a financial roadmap for lenders, assuring them of your income reliability and strengthening your prospects of securing a mortgage as a self-employed individual.

Building a Strong Credit History as a Self-Employed Individual

Maintaining a robust credit history is vital for all applicants, but it’s especially crucial for self-employed individuals. A good credit score demonstrates your financial responsibility and your ability to manage debt effectively.

Make sure to monitor your credit report regularly and address any issues promptly. Paying your bills on time, reducing outstanding debts, and avoiding new credit inquiries can help improve your credit score and increase your chances of approval.

Choosing the Right Mortgage Lender for Self-Employed

Selecting the right mortgage lender is a critical decision in your homeownership journey. Not all lenders have the same policies and requirements for self-employed applicants.

It’s essential to research and choose a lender with experience in working with self-employed individuals. They will understand your unique financial situation and offer products tailored to your needs, increasing your chances of approval.

Tips for Preparing Your Self-Employment Income Proof

Preparing self-employment income proof is a crucial step in securing a mortgage. Start by maintaining meticulous financial records, including bank statements, profit and loss statements, and tax returns, for at least two years. Consistency in your income documentation is key. Be ready to explain any fluctuations to your lender.

Consider hiring a certified accountant who specializes in self-employment income to ensure accuracy and compliance. Keep your personal and business finances separate, as commingling funds can create confusion for lenders. Lastly, be proactive in addressing any outstanding debts and improving your credit score to bolster your financial profile. By following these tips, you’ll present a strong case to lenders, increasing your chances of approval as a self-employed individual.

The Role of a Robust Business Plan in Mortgage Approval

A well-structured business plan can be a powerful asset when applying for a mortgage as a self-employed individual. Your business plan should outline your future income projections and strategies for business growth. This can help lenders gain confidence in your financial stability and repayment capability, even if your income is subject to fluctuations.

Managing Debt-to-Income Ratio Effectively

Your debt-to-income (DTI) ratio plays a crucial role in your mortgage approval. It represents the percentage of your monthly income that goes toward debt payments. Lenders prefer a lower DTI ratio, typically below 43%. To improve your DTI ratio, consider paying down existing debts or increasing your income. A lower DTI ratio makes you a more attractive candidate for mortgage approval.

Navigating Down Payments and Mortgage Insurance

For self-employed individuals, saving for a down payment can be a significant hurdle. While conventional mortgages typically require a 20% down payment, there are other options available, such as FHA loans with lower down payment requirements. Additionally, you may need to factor in mortgage insurance, which can be a part of your monthly mortgage payment. Understanding these costs and planning for them is essential for a successful mortgage application.

Case Studies ─ Success Stories of Self-Employed Homeowners

To illustrate the potential for self-employed individuals to secure mortgages successfully, let’s delve into a couple of real-life case studies. These stories showcase how determination, financial planning, and the right approach can lead to homeownership, even for those with non-traditional income sources.

Case Study 1 ─ Sarah’s Entrepreneurial Journey

Sarah, a self-employed graphic designer, dreamt of owning her own home. Despite facing income fluctuations, she meticulously documented her earnings and maintained a solid credit history. She partnered with a lender experienced in working with self-employed individuals who guided her through the process. With a well-crafted business plan and a clear demonstration of her financial stability, Sarah secured her mortgage and moved into her dream home.

Case Study 2 ─ Mark’s Real Estate Ventures

Mark, a self-employed real estate investor, had multiple income streams from rental properties and investments. While his income was variable, he consistently demonstrated positive cash flow and maintained a low DTI ratio. By partnering with a lender familiar with real estate professionals, Mark successfully obtained a mortgage that allowed him to expand his investment portfolio.

Empowering Self-Employed Individuals in Homeownership

Securing a mortgage as a self-employed individual may come with its set of challenges, but with careful planning, financial responsibility, and the right lender, it’s entirely achievable. Building a strong credit history, maintaining financial stability, and providing thorough documentation are the cornerstones of mortgage success. By following the strategies outlined in this guide, self-employed individuals can confidently pursue their homeownership dreams in 2024 and beyond. Remember, with determination and the right guidance, owning a home can be well within reach, regardless of your employment status.